Our Roadmap emphasises that ‘offsetting’ emissions should be used to reach this target only as a last resort – when it would otherwise be impossible to fully decarbonise essential certain activities. Offsets are not an alternative to emission reductions.

We recognise that ‘offsetting’ has sometimes been a controversial topic amongst climate experts. Our members are committed to only purchasing credible ‘offsets’ or ‘carbon credits’, and to ensuring they are transparent about how and when these are used.

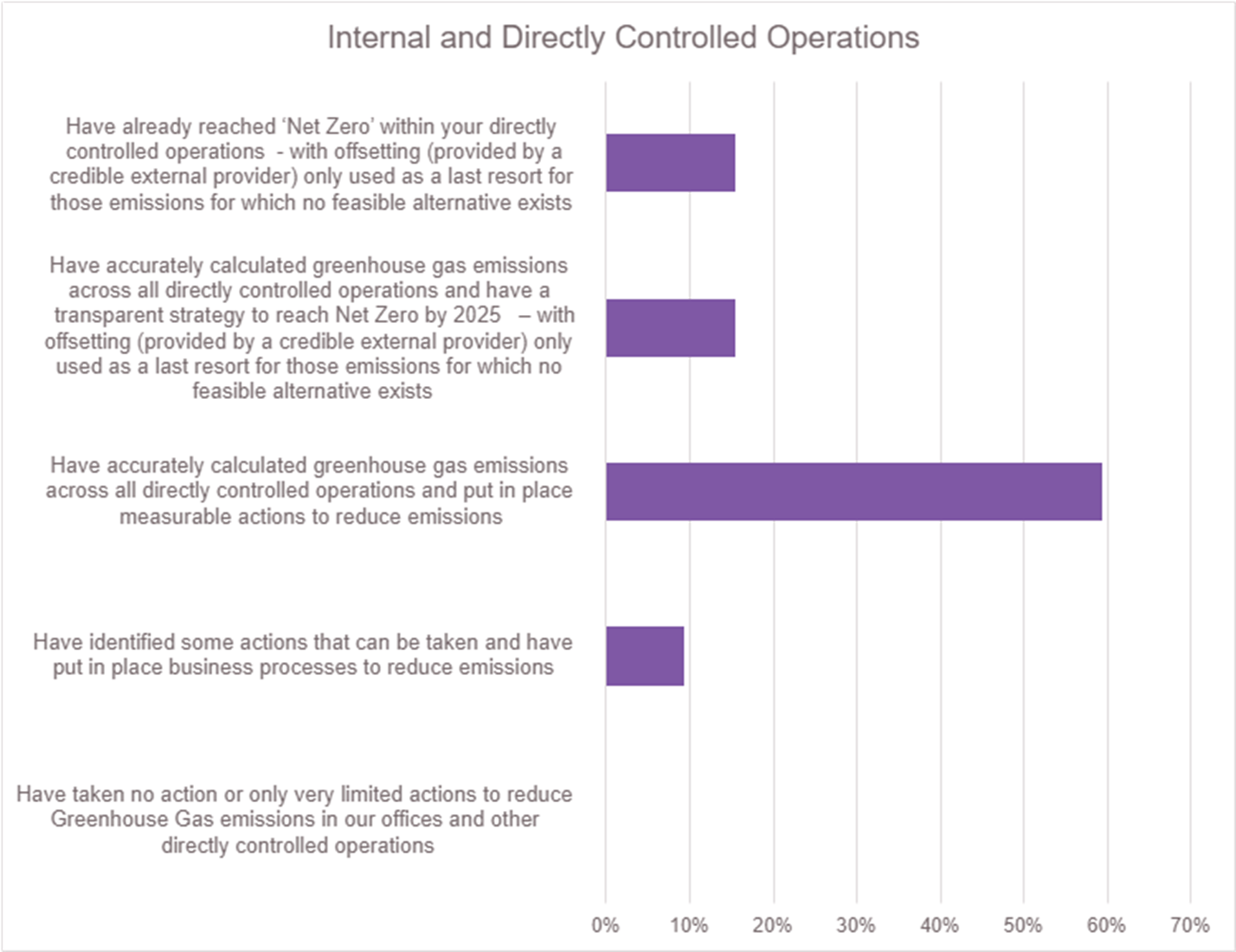

Examples of actions our members are taking to reduce GHG emissions linked to their internal operations include:

- Offering tools to individual employees to allow them to offset their business and personal travel

- Supporting UK and international tree planting, biodiversity and wetland forest restoration initiatives and carbon removal initiatives

- Partnership with deforestation initiatives supported by the UN’s REDD+ framework

- Innovative CO² removal – such as geothermal capture and conversion, biomass burial and waste conversion

- Purchase of renewable energy certificates

Our members are working with a wide range of organisations that provide Gold Standard and Verified Carbon Standard global offsetting projects. Examples of organisations that our members currently partner with include:

- Climateworks

- Ecologi

- Planetly

- Natural Capital Partners

- InterEarth

- Bio Restorative Ideas

- Oregon Biochar Solutions

- Climate Care

- Carbon Neutral Company

- InfiniteEARTH

- Energise

- Quantas Carbon Offset Programme

- One Carbon World

- Carbon Footprint

However, the purchase of ‘carbon credits’ can have a positive role to play in providing financing for environmental projects that may otherwise have struggled to raise investment.

It will also be important to continue to make carbon offsetting and voluntary carbon markets more effective. The Government’s forthcoming updated Green Finance strategy is an excellent opportunity to make the UK a world leader in Voluntary Carbon Markets.

The work of the Integrity Council for Voluntary Carbon Markets (ICVCM) and Voluntary Carbon Markets Integrity Initiative (VCMI) will be important to increase confidence in the supply of carbon credits. We also welcome the London Stock Exchange’s work to develop a platform for a robust voluntary carbon market.

A well-regulated market of innovative carbon credits should allow firms to be proud of the investments they are making (rather than seeing carbon credits as a ‘fine’) and drive a flow of investment to projects that are hard to finance under conventional structures.

We are committed to working closely with the initiatives looking to design standards for Voluntary Carbon Markets – in particular, to ensure that appropriate insurance is available to underpin these.

Supply Chain Emissions

We have published ‘Good Practice Guide on engaging with supply chains for Insurance and Long-Term Savings Providers’ .

This guidance has been developed by a working group of procurement experts from within our membership. It has been informed by working with Baringa and also through our ongoing collaboration with ClimateWise.

It represents the first stage of taking forward the four pro-active steps identified in our Roadmap.

Through this best practice guide, we aim to drive action on the first two of these four pro-active steps.

- Taking account of emissions reduction strategies and targets in supplier on-boarding

- Making sustainability a factor in decision making on suppliers

As our members often source services from the same suppliers, this consistency will create a strong incentive for more businesses across different parts of the economy to review their emissions and identify where they can make emission reductions.

Our guidance sets out expectations for engagement with larger businesses in our sector’s supply chain – where the provision of data and evidence on environmental impact and greenhouse gas emissions is already becoming more widespread through a combination of voluntary initiatives (including the Science Based Targets initiative (SBTi) and the UN Framework Convention on Climate Change (UNFCCC)’s Race To Zero campaign) and mandatory requirements, such as the UK’s implementation of the TCFD principles on a mandatory basis.

The guidance also sets out expectations for engagement with smaller businesses – where we recognise that the capacity to provide granular data and in-depth transition plans will be more limited. However, we intend to drive change in these businesses through a consistent approach from our members and alignment with the approaches developed specifically for SMEs by the SBTi and the SME Climate Hub.

Effective implementation of these practices will allow the sector to then focus on the third and fourth pro-active actions outlined in our Climate Change Roadmap – tracking and reducing emissions and simultaneously encouraging a circular economy.

Engagement with suppliers on the basis outlined in our Good Practice Guide should begin as soon as possible – many insurers are already actively engaging with their supply chain and other firms should therefore be able to learn from their experience and adopt the same goals.

By 2025, we expect this engagement to be a routine feature of procurement processes across the sector.

The aim of this engagement by our members should be to achieve one or more of the following longer-term objectives:

- to allow businesses within the Insurance and Long-Term Savings sector’s supply chain to provide the data on their own GHG Emissions that our sector is obliged to include within its own Scope 3 Emissions targets

- where appropriate, to allow individual Insurance and Long-Term Savings providers to consider incorporating performance on GHG emissions reductions into their competitive procurement processes (provided this allows ABI members to meet their contractual and legal obligations to policyholders, clients and third-party claimants)

- where appropriate, to make informed decisions on excluding certain businesses from supply chains where they have failed to make reasonable efforts to reduce their GHG emissions

We have recently recruited a secondee from one of our member firms who will be leading a project to drive further collaboration in this area across the sector.

We expect to be able to publish further updates on this within the next 12 months.