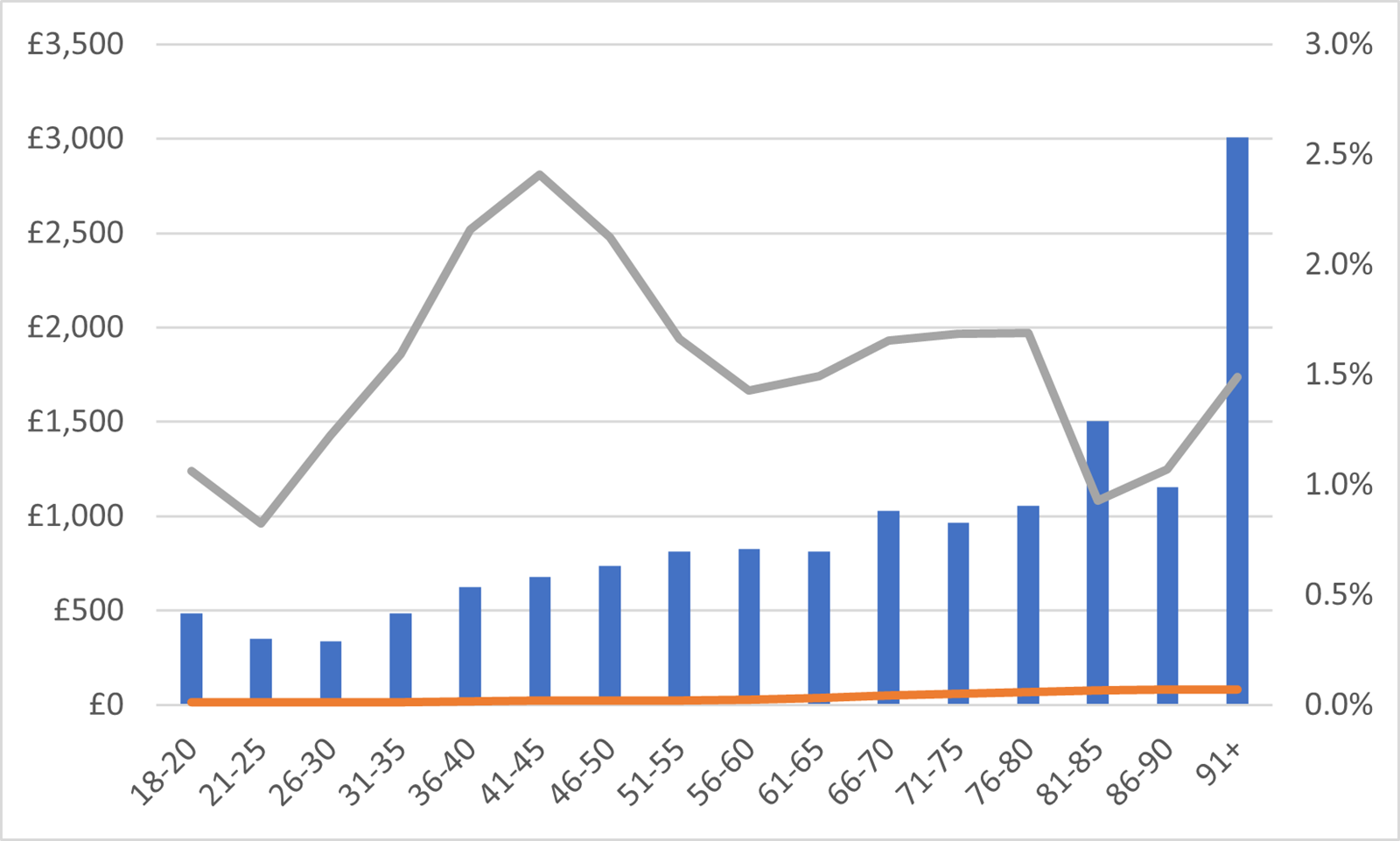

Why age is important to insurers when pricing travel insurance

Although travel insurance often includes valuable cover for things such as lost baggage, cancellations and disruption to holidays, it is fundamentally designed to cover the cost of emergency medical treatment needed when you are abroad (and to pay for special arrangements needed to return you home). For this reason, it is medically underwritten and so takes into account pre-existing medical conditions, age and the cost of treatment in the destination of travel - which can vary significantly.

Interestingly, older age groups are more likely to also have a pre-existing condition which in some cases may affect their premium and in general may be more likely to travel to destinations, such as the Caribbean, where the cost of treatment is significant. This does not mean that travel insurers assume that age is a proxy for either a pre-existing condition or destination of travel, with each asked for by insurers in their own right. Therefore, someone applying for insurance may see their premium increase purely based on the destination of travel, regardless of their age.