One size doesn’t fit all

28/02/2020

It is one of the generally accepted facts of the modern world that other than in the musical stylings of Frank Zappa, one size does not fit all. From exercise regimens to entertainment, people increasingly expect goods and services they receive to be tailored specifically to their own requirements. Pensions information should be no different. There are around 32.5 million people working and accruing pension entitlements in the UK (if you include state pension) and expecting them all to access pensions information in a uniform manner is misguided to say the least. This is the fundamental reason why I have always been opposed to the idea of a single pensions dashboard – the same thing that works for a 65 year old will probably not work for a 22 year old. Without meaning to sound like the stereotypical millennial snowflake I am, everyone is different, everyone is special and they deserve to have their needs met.

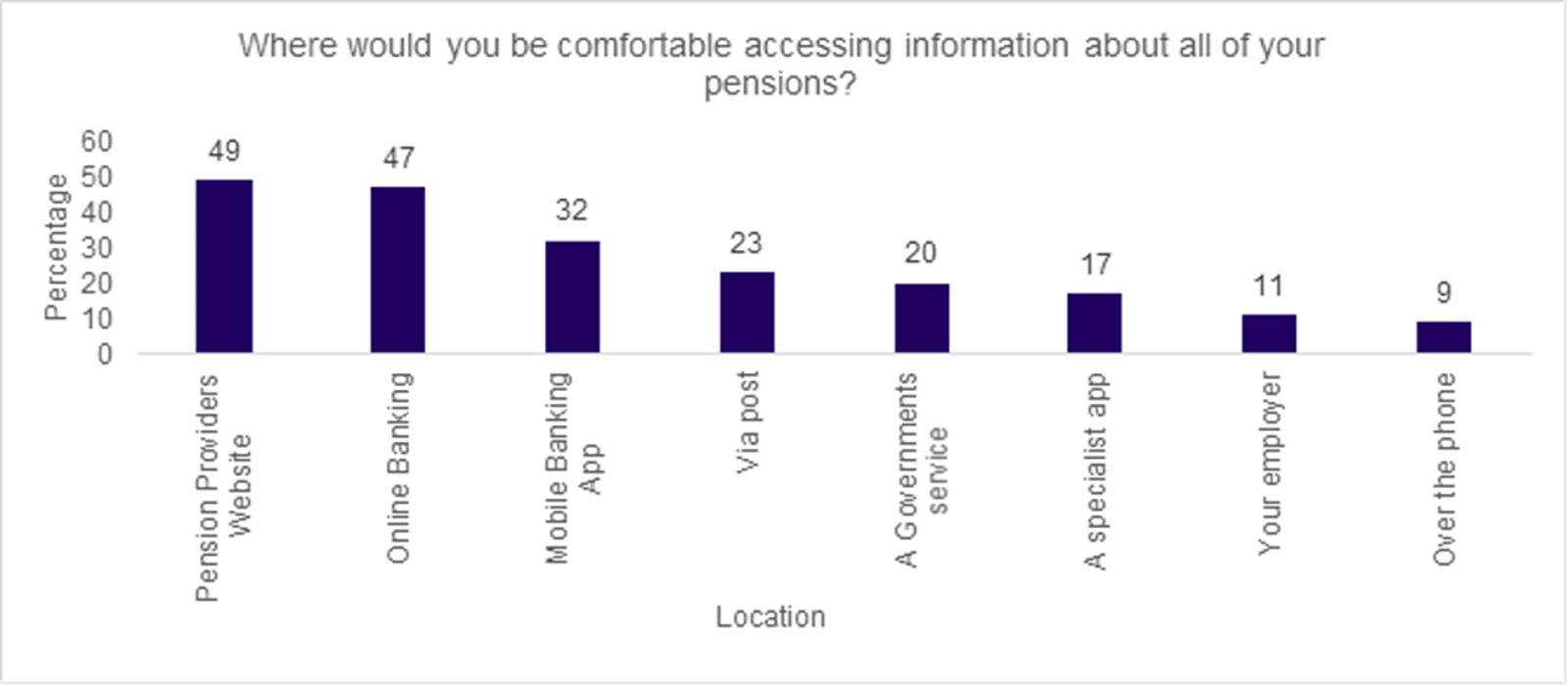

In order to validate this theory, we commissioned some polling to ask consumers where they would be comfortable accessing their pensions information and where they would find it convenient. Lo and behold there were substantial differences in the options selected by people with different characteristics. Whilst there were some differences by region and employment type, the most profound difference was by age. Our research found that:

- 60% of 25-34-year-olds would be comfortable viewing their pensions through their mobile banking app, in comparison to only 11% of those aged 65+.

- 20% aged 65+ comfortable receiving their pension data via post, in comparison to only 4% of 18-24-year-olds.

- 61% of those aged 55-64 with would find it most convenient to view their savings through their pension provider’s website, in comparison to 37% of 18-24-year-olds.

The overall landscape also reflected a diversity of opinions when it comes to where people would like to see their pensions information.

These findings to go to the heart of the issue: if you want people to engage with their pensions then you need to make it easy for them. Parts of the pensions industry have a paternalistic tradition that sometimes takes the form of talking down to people. This has frequently taken the form of one letter a year and a view that it’s best for the average person on the Clapham omnibus not to engage at all anyway. Pensions Dashboards are a once in a generation opportunity to shake up this dynamic by giving people the ability to access their information in a safe place that suits them. For some people this will be the Money and Pensions Service, for others it’ll be their provider or their banking app. It could be another body like a consumer group or trade union. If you choose to only cater to one of these segments, don’t be surprised when very few people use the end product.

Pensions Dashboards, along with open banking and the wider concept of open finance, are at their core about self-knowledge. At the moment, most people in the UK muddle through their financial lives with little information and knowledge, meaning they don’t get the most out of the assets they have. By giving people access to their information when they want, in the way that they choose, we can change this and empower people to live better more financially healthy lives.